Calculate DBR, what does it mean, and why should you care about it in the UAE? The Debt Burden Ratio (DBR) of your credit card or loan application is the most important element that will ensure you are approved or rejected by UAE banks. In plain English, it depicts the extent to which your monthly earnings have been allocated to settle debts like loans, mortgages, and credit card payments.

In this blog, I will guide you step by step on how to calculate DBR for a credit card in the UAE, what formula you can use, and what happens if your DBR exceeds the 50% limit set by the UAE Central Bank.

What Is DBR in the UAE?

When you apply for a credit card, loan, or any type of financing in the UAE, the first thing banks and lenders look at is your DBR, Debt Burden Ratio. It’s a financial indicator that tells how much of your monthly income goes toward paying your existing debts. In other words, it reflects how much of your earnings are already committed before you even think about taking on new credit.

In the UAE, this concept is not just a guideline; it’s a mandatory financial assessment tool set by the Central Bank of the UAE. Every licensed bank must calculate its DBR before approving any new lending facility.

Why DBR Is So Important in the UAE

In the UAE, the Central Bank has set clear regulations regarding the maximum DBR limit. According to the UAE Central Bank rules:

- The maximum DBR allowed is 50% of your monthly income.

- This means that half of your income can go toward loan and credit card payments, while the other half must remain available for your living expenses.

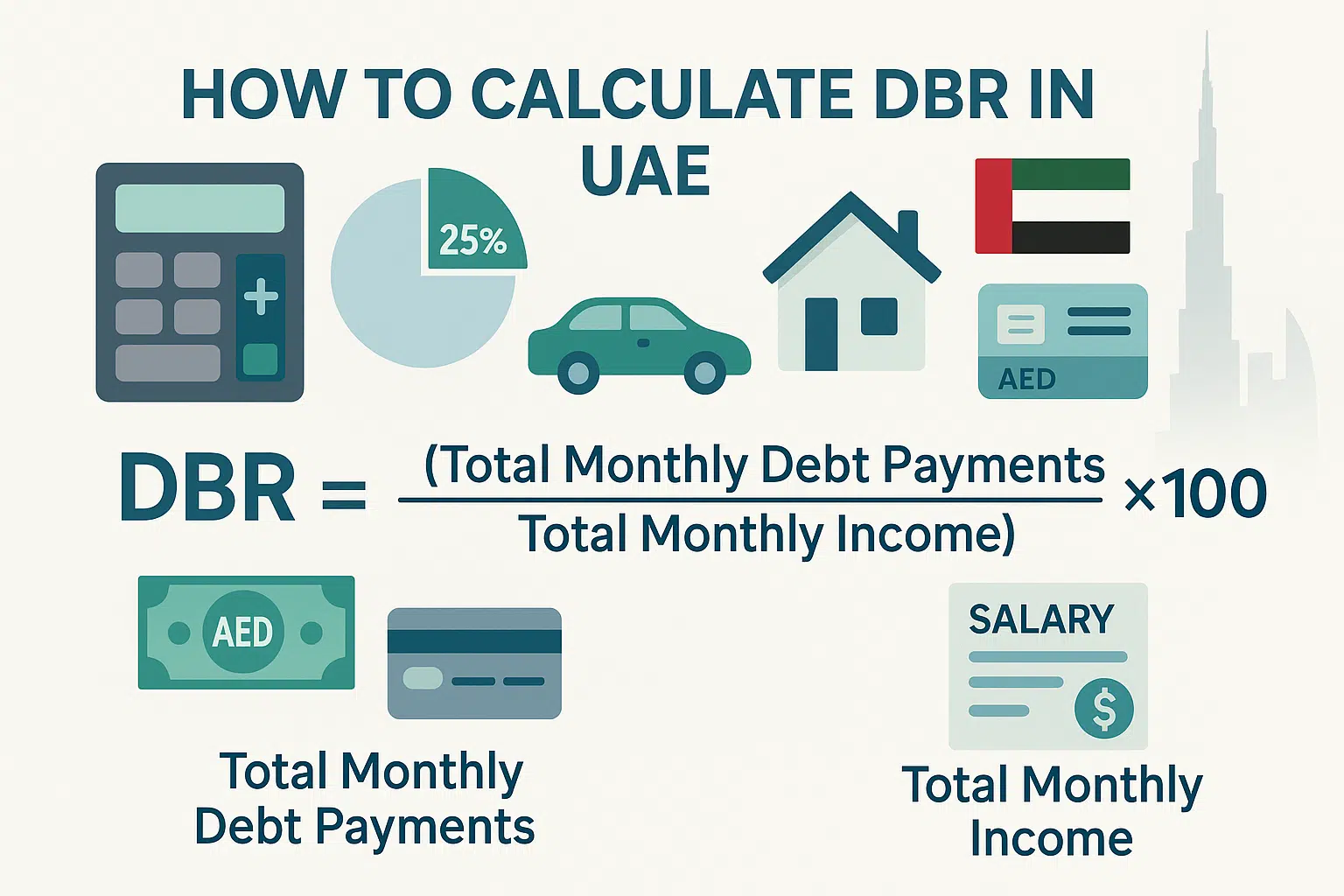

Formula: How to Calculate DBR in the UAE

Your Debt Burden Ratio (DBR) is calculated according to the following formula:

DBR = (Total Monthly Debt Payments ÷ Total Monthly Income) × 100

Where:

- Total Monthly Debt Payments: All payments of personal loans, auto loans, mortgages, and 5 per cent of your total credit limits.

- Total Monthly Income: Your gross monthly income (salary, allowances, rental income, etc.).

Example: Calculate DBR in the UAE

| Financial Details | Description | Monthly Amount (AED) |

|---|---|---|

| Monthly Income | Your total gross monthly salary (before deductions) | 12,000 |

| Personal Loan Payment | Fixed monthly instalment | 1,800 |

| Car Loan Payment | Auto financing instalment | 1,000 |

| Credit Card Limit | AED 10,000 × 5% (bank assumes 5% as monthly obligation) | 500 |

| Total Monthly Debt Payments | 1,800 + 1,000 + 500 | 3,300 |

What Happens If Your DBR exceeds 50%?

This is one of the most common concerns among people applying for credit cards in the UAE.

1. Application Rejection

In case your DBR crosses 50%, banks usually reject your new credit card or loan application. This is because you’re already using more than half of your income to pay off debts, leaving little margin for new financial commitments.

2. Reduced Credit Limit

Sometimes, instead of rejecting your application, banks may offer you a smaller credit limit to ensure your DBR stays within a safe range.

3. Negative Impact on Credit Score

High DBR means that it is highly exposed to debt, which can negatively impact your credit. That means future credit applications may also face difficulties.

4. Difficulty in Loan Top-Ups

In case you have existing loans and want to apply for a top-up, your bank will first check your DBR. If it exceeds 50%, they will likely decline the increase.

5. Financial Stress

In addition to approvals and scores, a large DBR will result in less disposable income, which may lead to financial stress and postpone your long-term objectives of saving, investing, or purchasing property.

Read Also: Urgent: How to Apply Single Exit-Re-Entry Visa Today

Methods to Calculate DBR in the UAE

There are mainly two effective ways to calculate your DBR accurately.

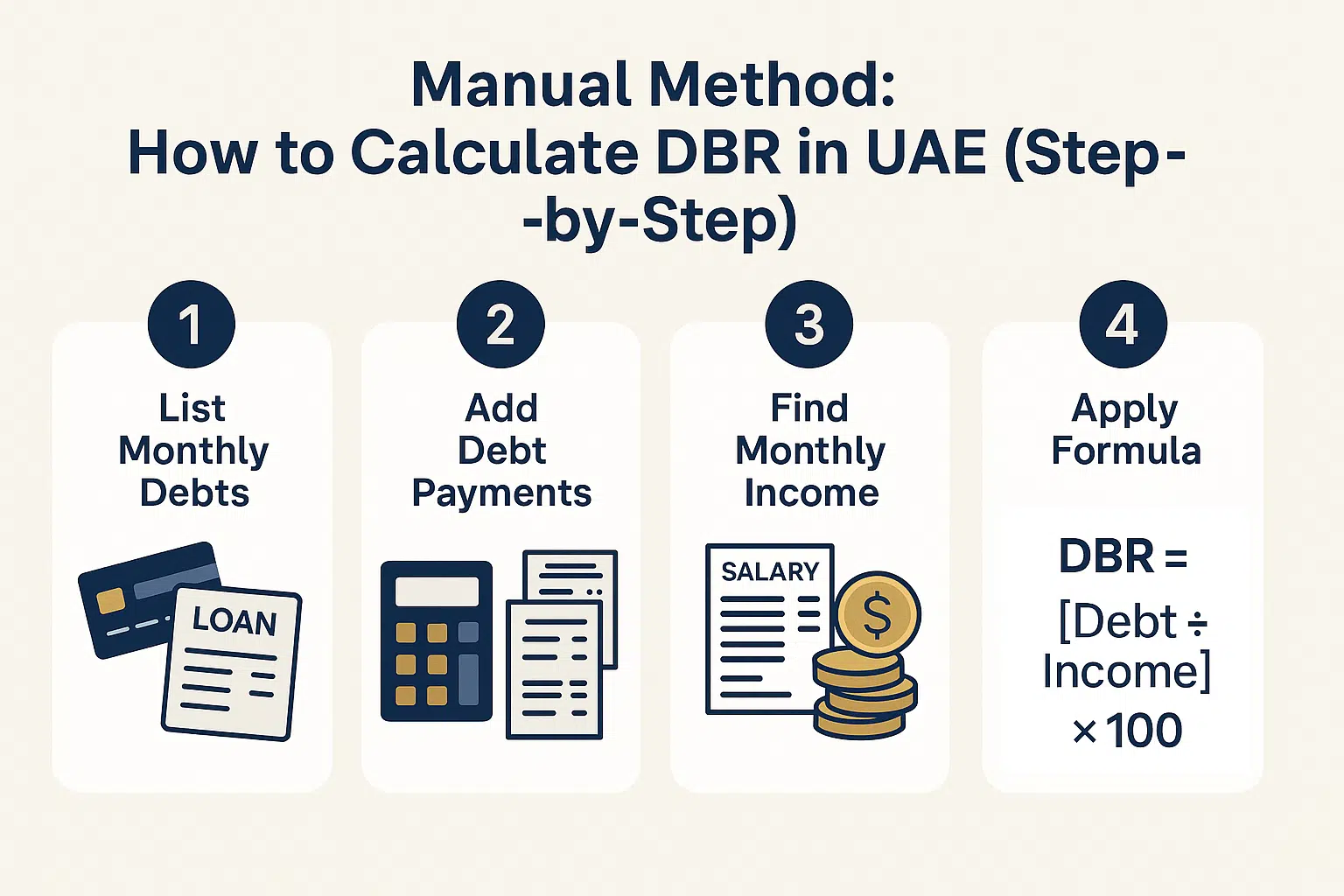

1. Manual Method

You can calculate it manually using the formula we discussed earlier. Here’s what you should do:

Step 1: List All Your Monthly Debts

Include:

- Personal loans

- Car loans

- Home loans

- Credit cards (5% of total limits)

- Any other regular debt payments

Step 2: Add Up Total Monthly Debt Payments

Add these together: this is what you are in debt to every month.

Step 3: Determine Your Total Monthly Income

Includes full gross salary, rent income (where applicable), and other proven sources of income.

Step 4: Apply the Formula

Use:

DBR = (Total Monthly Debt Payments ÷ Total Monthly Income) × 100

This gives your DBR percentage.

2. Online DBR Calculator on Our Website

To make things much easier, I’ve also created an online DBR calculator on our website.

You simply need to:

- Enter your monthly income.

- Add your loan installments and credit card limits.

- Click “Calculate”.

In seconds, you’ll get your DBR percentage, showing exactly how close you are to the UAE Central Bank’s limit of 50%.

Tips: DBR for Credit Card Approval

1. Reduce Outstanding Loan Balances

Try to pay off small or short-term loans before applying for new credit. This immediately reduces your total monthly debt obligations, thus lowering your DBR.

2. Avoid Applying for Multiple Cards at Once

Each new application will result in possible debt and have an impact on your credit score. There should be space between applications; concentrate on one application at a time.

3. Increase Your Income Sources

When applying, ensure that you declare any side income, like rent, freelancing, or investments. Banks use all verifiable income to compute your DBR.

4. Transfer High-Interest Debts

When you possess more credit cards, you may transfer the unpaid bills to a low-interest card to save on monthly payments.

FAQs

What does DBR mean in the UAE?

It is the Debt Burden Ratio, or what proportion of your income is allocated to loan and credit card payments.

What is the DBR limit for the UAE residents?

The UAE Central Bank allows a maximum DBR of 50% of your total monthly income.

What if my DBR is above 50%?

Your credit card or loan may be rejected until you lower your existing debt or increase your income.

Read Also: 4 Free Ways to Check FAB PPC Card Balance

Final Words

One of the smarter financial practices you can acquire is to know how to compute DBR in the UAE. Your Debt Burden Ratio is not just another percentage; it is the reflection of your income and debt management. It indicates that lenders can trust you to use credit wisely when your DBR does not exceed the 50% threshold of the UAE Central Bank.

I always encourage you to take control of your finances by checking your DBR regularly. Use the online DBR calculator on our website to instantly see where you stand before applying for any credit product.