- What Are Credit Card Rules?

- Minimum Income Requirement

- Credit Card Without Salary in the UAE

- Credit Limit Cap Rule (The 50% Income Law)

- Credit Cards Are Treated as “Additional Facilities”

- Interest and Grace Period Rules

- Rules for Non-Residents in the UAE

- No Forced Credit Card Upgrade

- Fees Control in the UAE

- Debit Cards for Low-Eligibility Customers

- Credit Card Rules for Expats vs UAE Nationals

- How Your Credit Score Affects Your Card Approval

- Common Mistakes I See People Make

- How to Choose the Right Credit Card in the UAE

- Comparison Table: Key UAE Credit Card Rules

- Frequently Asked Questions

- Final Words

Do you know the regulations of the credit card in the UAE? Many residents and expatriates become confused about eligibility, limits, and fees before applying, which may result in penalties or the loss of opportunities.

To enjoy your credit card safely and make the most of it, you should understand Central Bank regulations, minimum income requirements, interest regulations, and restrictions on residents and non-residents.

In this complete guide, I will provide all that you should know about credit card regulations in the UAE, including eligibility and secured cards, fees, the rules of repayment, and some tips from experts.

What Are Credit Card Rules?

Credit card rules refer to the official stipulations and policies by banks and the Central Bank to regulate the issuance, use, and management of credit cards. These regulations are to protect the financial security, prudent lending, and disclosure on the part of the cardholder and the bank.

The UAE credit cards are regulated by:

- Central Bank of the UAE (CBUAE)

- UAE Banking Regulations

- Consumer Protection Laws

- Al Etihad Credit Bureau (AECB)

They would stick to the national lending standards, which are in place to ensure that you and the financial system are safeguarded.

Minimum Income Requirement

What Is the Official Salary Rule?

In the UAE, to obtain a regular credit card, one needs:

You have to earn a minimum of AED 60,000 every year (around AED 5000 annually).

This rule applies to:

- UAE residents

- Expatriates

- Salaried employees

This is one of the least understood rules in my case. Individuals would submit their applications with a lower income and ask why their application is rejected, even when they have a good banking history.

Why This Rule Exists

This limit is imposed by the UAE Central Bank to:

- Reduce consumer debt

- Prevent financial instability

- Make borrowers have the ability to repay balances reasonably.

What Happens If You Don’t Meet the Salary Requirement?

When you are earning less than this amount, the banks will not be able to loan you a normal unsecured credit card. But that does not imply that you are totally locked out.

Credit Card Without Salary in the UAE

Can You Get a Credit Card Without Meeting Income Requirements?

Yes—but only under strict conditions.

Assuming that your income falls below AED 60,000 per year, however, you can still obtain a credit card provided:

- You put down a fixed deposit of AED 60,000 minimum.

- That deposit is considered financial security by the bank.

This is referred to as a secured credit card.

How Secured Credit Cards Work in the UAE

You do not have to borrow money from the bank. You lend yourself against your deposit.

Important Rule You Must Know

Your total:

- Credit card limit

- Plus any other credit facilities

Cannot exceed 50% of your pledged deposit

So if you deposit AED 60,000, your maximum credit access is usually capped at AED 30,000.

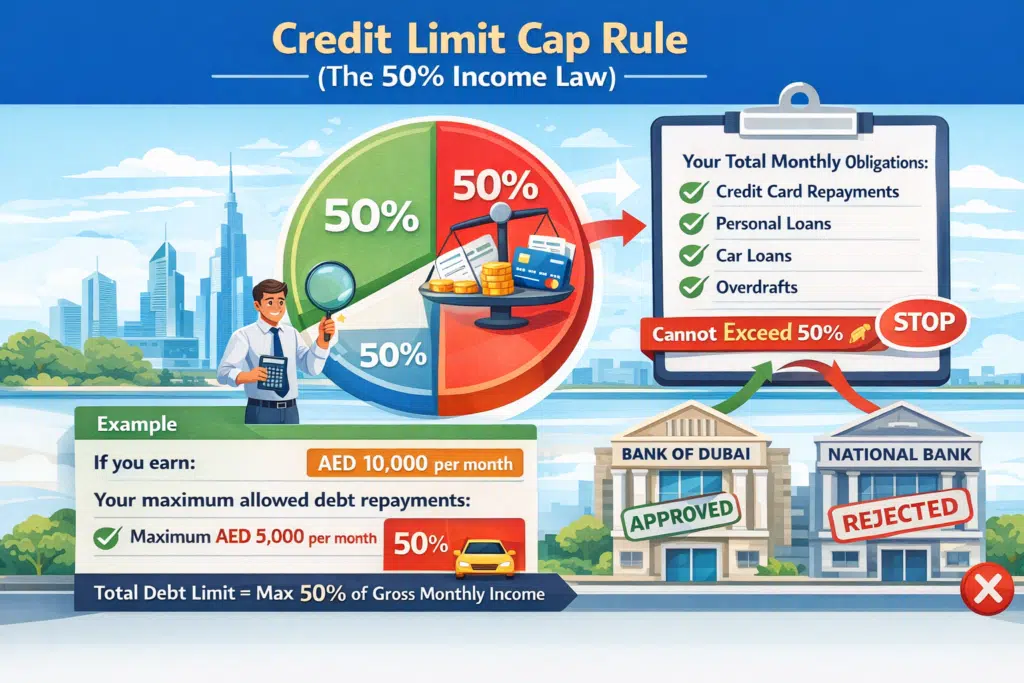

Credit Limit Cap Rule (The 50% Income Law)

This is one of the strongest financial protections in the UAE, and many cardholders don’t realize it exists.

What the 50% Rule Means

Your total monthly financial obligations:

- Credit card repayments

- Personal loans

- Car loans

- Overdrafts

Must not go over 50% of your pledged deposit.

Example

If you earn:

- AED 10,000 per month

Your total allowed debt repayments:

- Maximum AED 5,000 per month

Whilst one bank may approve you, a second bank will have to disapprove you in case your total obligations are above this limit.

Credit Cards Are Treated as “Additional Facilities”

What Banks Legally Classify Your Card As

A credit card in the UAE is regarded as:

Additional credit facility

This means:

- It is not recorded as something independent of your loans.

- It continues to have an impact on your score on affordability.

- Still, it counts towards the 50% rule.

Therefore, when your salary rises, banks have to:

- Recalculate your total obligations

- Reassess your financial capacity

- Evaluate your credit bureau records

Unlimited cards are not necessarily a sign of a high income.

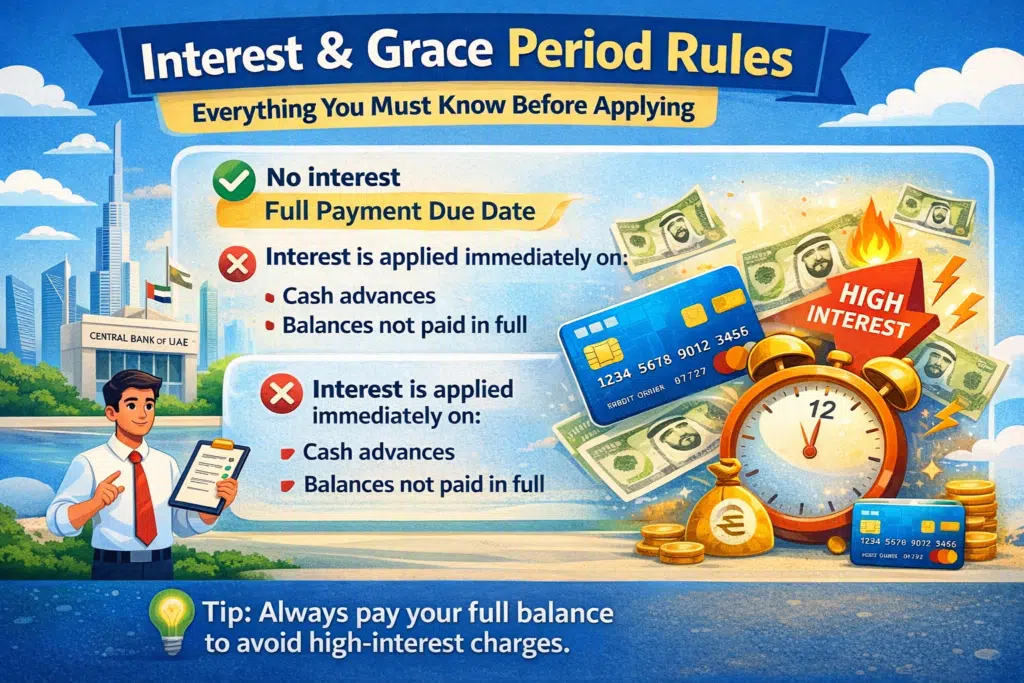

Interest and Grace Period Rules

When Banks Cannot Charge Interest

You will not be interested in the case:

- You pay the full outstanding amount

- You pay it before the due date

This is referred to as the grace period and is one of the biggest incentives for using a credit card responsibly.

When Interest Starts Immediately

The banks are permitted to charge interest on:

- Cash advances

- Partial payments

- Carried-over balances

In my case, cash withdrawals lead to trouble for most of the users, as the interest begins to count as of day one and not at the end of the billing cycle.

Read Also: How to Use DU Quick Recharge Online in UAE (2026)

Rules for Non-Residents in the UAE

Can Non-Residents Get Credit Cards?

Yes, however, banks are required to be very careful.

What Banks Must Do

They are required to:

- Track non-resident data separately

- Monitor spending behavior closely

- Apply stricter risk assessments

Issuance is not prohibited, but it is under strict regulation by regulators.

Practical Reality

From what I’ve seen:

- Limits are usually lower

- Documentation is stricter

- Approval time is longer

No Forced Credit Card Upgrade

This is a rule that safeguards you in a greater way than you think.

What Banks Are Not Allowed to Do

They cannot:

- Increase your credit limit

- Upgrade your card (Classic → Gold → Platinum)

- Change your card type

Without your explicit consent

What Counts as Consent?

Banks must get:

- Written confirmation

- Email approval

- Or SMS verification

If you did not concur, the upgrade is not of the law.

Fees Control in the UAE

Can Banks Add New Fees?

No, not without Central Bank approval.

What Banks Must Follow

- Fees must be transparent

- Charges cannot be applied retroactively

- Terms must be disclosed clearly

This is to say that when a bank just goes ahead and adds a fee annually, they have to inform you and remain within the regulatory capacity.

Debit Cards for Low-Eligibility Customers

What Happens If You Don’t Qualify for a Credit Card?

Banks are encouraged to:

- Offer debit cards instead

- Reduce consumer debt exposure

- Promote safer spending behavior

It is a regulation-by-regulation suggestion – not merely a bank policy.

Credit Card Rules for Expats vs UAE Nationals

Most rules are equal, but there is a practical difference.

Expats

Usually need:

- Salary certificate

- Employment contract

- Emirates ID

- Bank statements

UAE Nationals

May receive:

- Higher flexibility

- Faster approvals

- Banking initiatives sponsored by the government.

But still, the rule of 50 percent works on all people.

How Your Credit Score Affects Your Card Approval

Banks check your data with:

- Al Etihad Credit Bureau (AECB)

They look at:

- Payment history

- Loan exposure

- Missed payments

- Outstanding debt

Even if you meet salary rules, a poor credit record can block approval.

Common Mistakes I See People Make

From years of reviewing banking cases, these are the most common errors:

- Applying for multiple cards at once

- Ignoring cash advance interest

- Not reading the fee structures

- Assuming salary alone guarantees approval

- Missing payment due dates

Any one of these can hurt your credit profile.

How to Choose the Right Credit Card in the UAE

Before applying, ask yourself:

- Do I pay balances in full every month?

- Do I need travel rewards or cashback?

- Can I comfortably meet repayment rules?

- Am I close to the 50% limit?

A card should serve your lifestyle—not control it.

Comparison Table: Key UAE Credit Card Rules

| Rule | Requirement | Example |

|---|---|---|

| Minimum Income | AED 60,000/year | Cannot get regular card without this |

| Secured Card | Deposit ≥ AED 60,000 | Credit limit ≤ 50% of deposit |

| Credit Limit Cap | ≤ 50% of gross monthly income | AED 10,000 income → max repayment AED 5,000 |

| Interest | Full payment = no interest | Cash advance = interest applied immediately |

| Upgrades | Requires explicit consent | No auto-upgrades |

| Fees | Central Bank approval required | No retroactive fees |

| Non-Residents | Issuance allowed but monitored | Extra documentation may be needed |

Frequently Asked Questions

What is the minimum salary for a credit card in the UAE?

AED 60,000 per year (≈ AED 5,000 per month). Below this, only secured cards are allowed.

Can I get a credit card without a salary?

Yes, if you deposit a minimum of AED 60,000 as collateral with the bank.

What happens if I miss a credit card payment?

Late payment fees are applied, and interest may be charged on the outstanding balance.

Can banks force a card upgrade?

No, the Central Bank mandates explicit consent for any upgrades.

Are fees fixed for all credit cards?

Fees must comply with Central Bank rules and cannot be applied retroactively.

Read Also: How to Contact du Customer Care UAE (2026 Update)

Final Words

Navigating credit card rules in the UAE can seem complicated, but understanding the minimum income requirements, secured card options, credit limits, fees, and consent rules will make it easy to manage your finances responsibly.

Always follow these rules to:

- Avoid penalties and unnecessary fees

- Maintain a healthy credit score

- Use your credit card as a smart financial tool

Start with a card you qualify for, follow these guidelines, and you’ll enjoy all the benefits without falling into debt.